M&A Index Poland

2 kwartał 2015

54

łączna liczba transakcji

1.6 mld

wartość największej transakcji (PLN)

31%

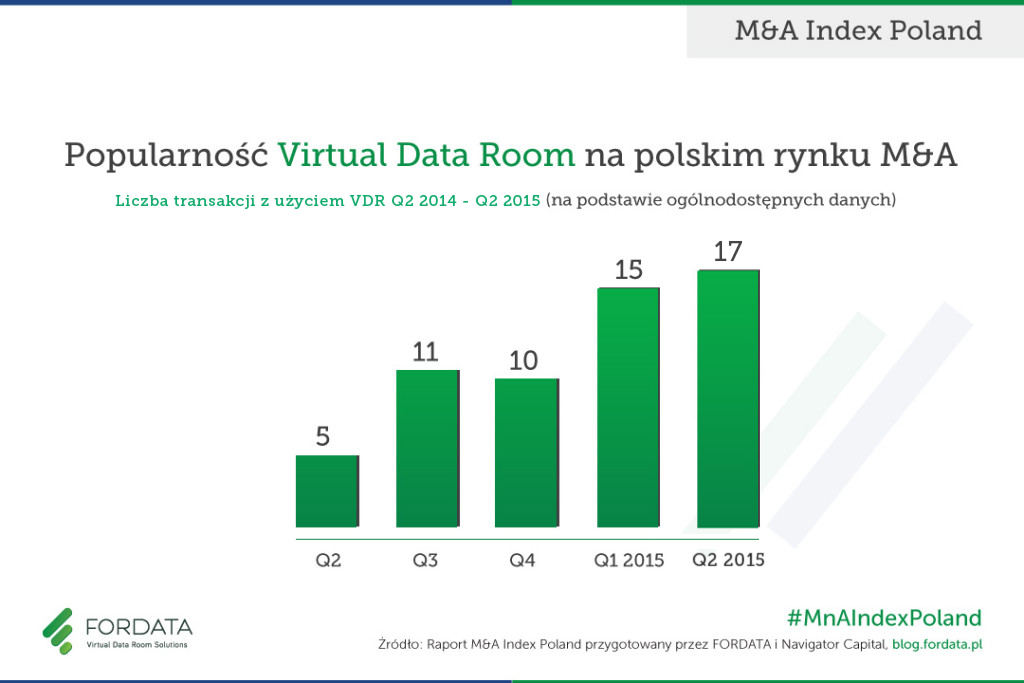

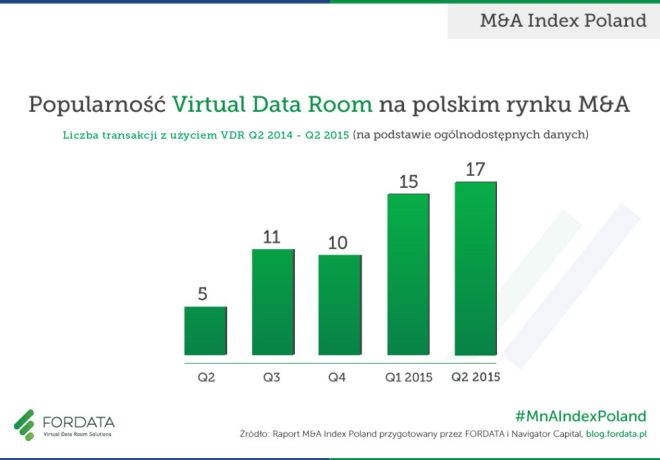

popularność Virtual Data Room

Utrzymuje się trend wykorzystania systemu Virtual Data Room podczas procesów transakcyjnych. Z dostępnych danych wynika, że w drugim kwartale 2015 r. 17 spośród 54 transakcji zostało zorganizowanych z użyciem systemu VDR (co stanowi kolejny wzrost, o 13% w stosunku do poprzedniego kwartału). Jedną ze spółek, która ujawniła informację o użyciu VDR był fundusz Enterprise Investors, który sprzedawał NordGlass, wiodącego europejskiego producenta szyb dla branży motoryzacyjnej. Zdaniem CEO NordGlass, Grzegorza Łajcy "Wykorzystanie dedykowanego narzędzia FORDATA VDR usprawniło proces sprzedaży udziałów".

Chcesz wymienić się wiedzą, podyskutować, zadać pytanie?

Maria Kotwis expert FORDATA

Poprzednie raporty fuzji i przejęć w Polsce

![]()

Jest czołowym dostawcą usługi Virtual Data Room w Polsce i w regionie CEE. Rozwiązanie FORDATA VDR wspiera największe transakcje M&A, IPO, inwestycje Private Equity i prywatyzacje.

W oparciu o autorskie systemy informatyczne, bazujące na technologii Virtual Data Room, pomaga klientom w zarządzaniu dokumentami i komunikacją podczas złożonych procesów transakcyjnych.

Współpracuje z liderami branż, w tym największymi firmami doradczymi, kancelariami prawnymi, bankami, czy funduszami PE/VC z całego świata. FORDATA zrealizowała dotychczas ponad 500 transakcji podnosząc bezpieczeństwo i efektywność projektów o łącznej wartości ponad 40 mld PLN.

![]()

Wraz z Domem Maklerskim Navigator jest czołowym niezależnym doradcą finansowym dla przedsiębiorstw specjalizującym się w transakcjach M&A oraz publicznych i prywatnych emisjach akcji i obligacji. W ciągu ostatnich lat Grupa Navigator zrealizowała ponad 35 transakcji różnego typu.

Partnerzy Navigator przeprowadzili transakcje o łącznej wartości ponad 6,2 mld PLN. Współpraca z międzynarodową siecią firm doradczych zrzeszonych pod szyldem Pandion Partners pozwala skutecznie obsługiwać transakcje międzynarodowe.

Navigator Capital wraz z Domem Maklerskim Navigator zajmują wysokie pozycje w niezależnych rankingach oceniających aktywność podmiotów doradczych na rynku polskim.