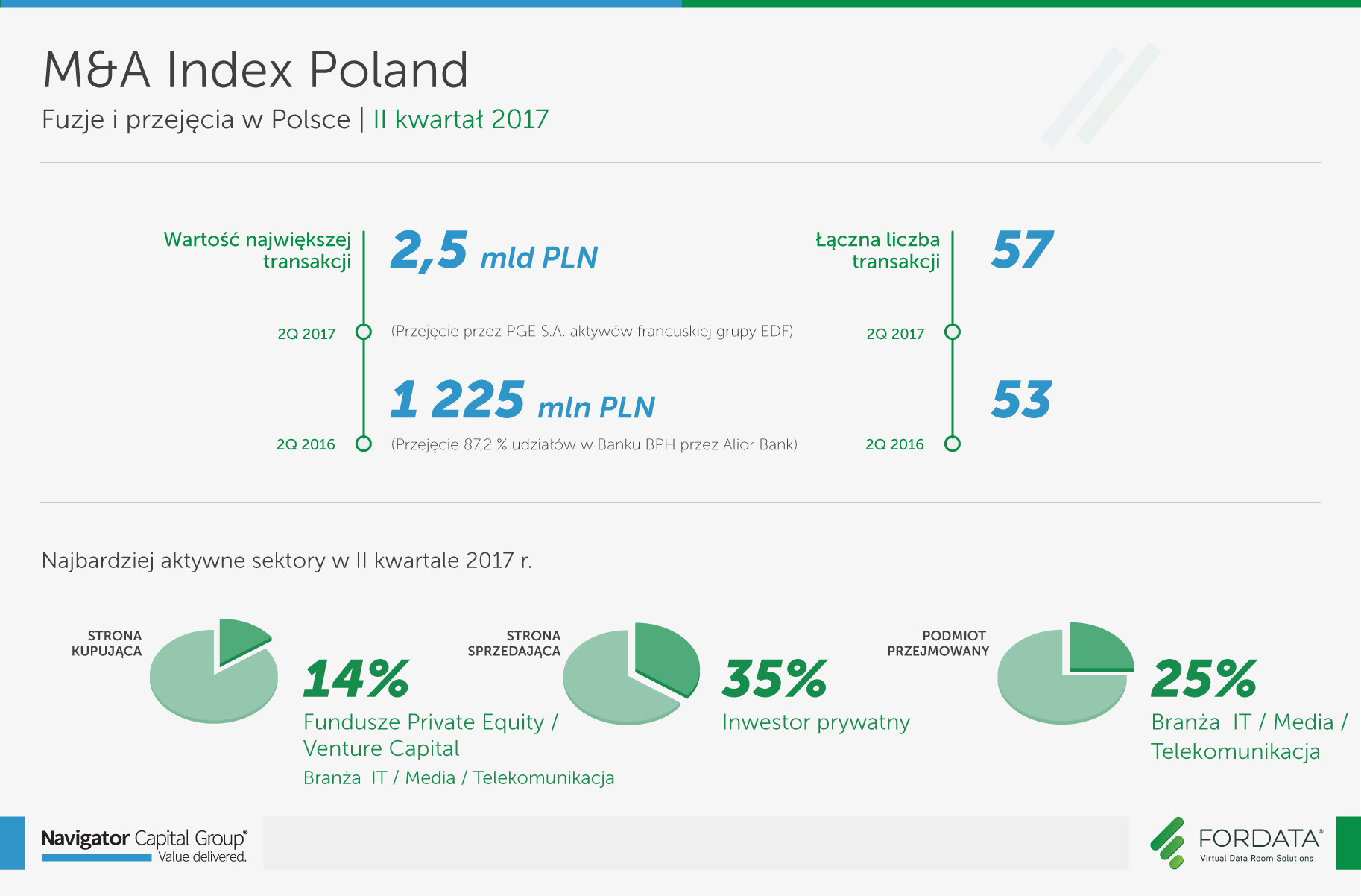

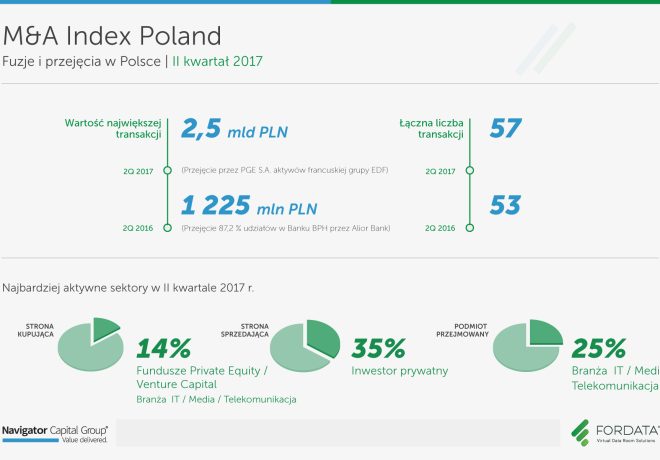

M&A Index Poland

2 kwartał 2017

57

łączna liczba transakcji

2.5 mld

wartość największej transakcji (PLN)

Widziany przypływ zagranicznych inwestorów do Polski, w tym nowych funduszy, jest wynikiem zmian, które zaszły w Europie i na świecie. Wiele rynków się zamknęło. Niepewny jest rynek brytyjski (Brexit, spadek funta), Turcja przestała być atrakcyjna, zamknięty jest też rynek rosyjski. Ilość kapitału się nie zmniejszyła, ale rynki się zawęziły, więc kapitał kieruje się tam, gdzie jest relatywnie bezpiecznie. Pieniądze, które mogły być zainwestowane na innych rynkach wpływają na nasz. Inwestycjom w Polsce niewątpliwie sprzyja sytuacja makroekonomiczna, która jest stabilna i zdecydowanie lepiej postrzegana niż bezpośrednio po wyborach w 2015 r., ale także wzrost gospodarczy i dobrze funkcjonujący system bankowy. Ryzyko inwestycyjne postrzegane jest podobnie jak w krajach Europy Zachodniej. To co studzi entuzjazm inwestorów to wprowadzane od kilkunastu miesięcy zmiany prawne, oceniane przez wielu ekspertów jako szkodzące gospodarce, a ponadto niekonstytucyjne. Dlatego też inwestorzy bardzo monitorują nasz rynek i sprawdzają każdą informację w prasie zagranicznej na temat sytuacji prawno-ekonomicznej w Polsce. Prognozujemy, że kapitał polski coraz siniej zacznie przejmować spółki w Europie. Tu będą obserwowane także duże transakcje. Kapitał w Polsce jest, ponad bilion złotych oszczędności w gospodarstwach domowych, na lokatach. Kwestia czasu i dobrych chęci, żeby go w końcu zainwestować. W 2 kwartale 2017 było już 10 takich transakcji – kupowaliśmy głównie na zachodzie (Niemcy, Francja).

Chcesz wymienić się wiedzą, podyskutować, zadać pytanie?

Alicja Kukla-Kowalska expert FORDATA

Poprzednie raporty fuzji i przejęć w Polsce

![]()

Jest czołowym dostawcą usługi Virtual Data Room w Polsce i w regionie CEE. Rozwiązanie FORDATA VDR wspiera największe transakcje M&A, IPO, inwestycje Private Equity i prywatyzacje.

W oparciu o autorskie systemy informatyczne, bazujące na technologii Virtual Data Room, pomaga klientom w zarządzaniu dokumentami i komunikacją podczas złożonych procesów transakcyjnych.

Współpracuje z liderami branż, w tym największymi firmami doradczymi, kancelariami prawnymi, bankami, czy funduszami PE/VC z całego świata. FORDATA zrealizowała dotychczas ponad 500 transakcji podnosząc bezpieczeństwo i efektywność projektów o łącznej wartości ponad 40 mld PLN.

![]()

Wraz z Domem Maklerskim Navigator jest czołowym niezależnym doradcą finansowym dla przedsiębiorstw specjalizującym się w transakcjach M&A oraz publicznych i prywatnych emisjach akcji i obligacji. W ciągu ostatnich lat Grupa Navigator zrealizowała ponad 35 transakcji różnego typu.

Partnerzy Navigator przeprowadzili transakcje o łącznej wartości ponad 6,2 mld PLN. Współpraca z międzynarodową siecią firm doradczych zrzeszonych pod szyldem Pandion Partners pozwala skutecznie obsługiwać transakcje międzynarodowe.

Navigator Capital wraz z Domem Maklerskim Navigator zajmują wysokie pozycje w niezależnych rankingach oceniających aktywność podmiotów doradczych na rynku polskim.