M&A Index Poland

3 kwartał 2016

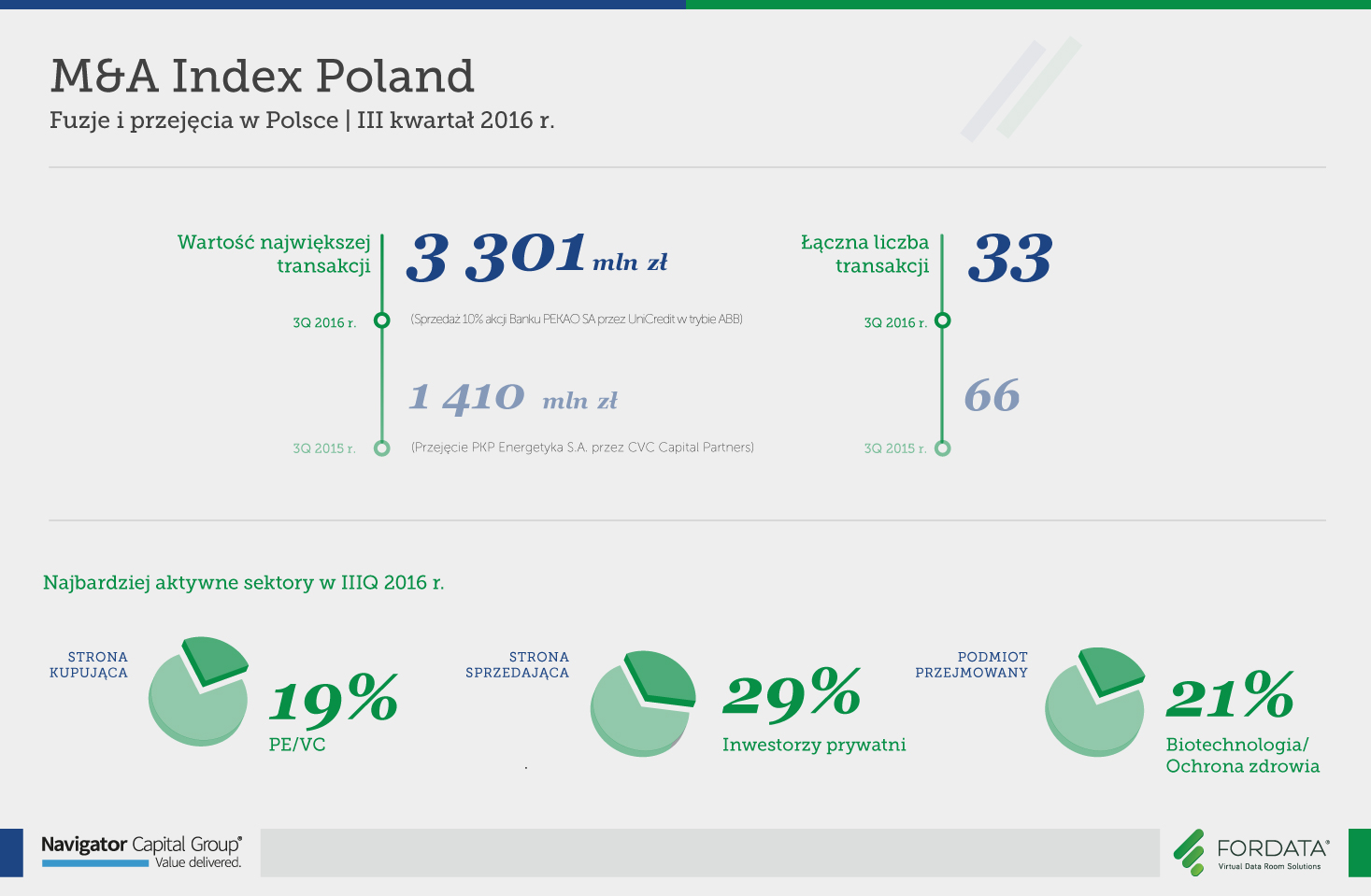

33

łączna liczba transakcji

3.3 mld

wartość największej transakcji (PLN)

21%

popularność Virtual Data Room

Z dostępnych danych wynika, że w tym kwartale Virtual Data Room został użyty podczas 7 transakcji. Obserwacja rynku pozwala jednak założyć, że transakcji zorganizowanych z użyciem VDR było więcej, jednak niestety nie wszystkie firmy zdecydowały się poinformować o tym rynek.To co możne studzić entuzjazm inwestorów na całym świecie to Brexit i wciąż niepewność dotycząca skutków jakie wywrze na UE. Niepewność widoczna jest na całym świecie. Poza rezultatem referendum w Wielkiej Brytanii, niepewność wywołują przewidywane od dłuższego czasu spowolnienie wzrostu gospodarczego Chin, kryzys migracyjny w Europie, a także, wybory w Stanach Zjednoczonych i zaostrzanie w wielu krajach polityki podatkowej względem korporacji.

Chcesz wymienić się wiedzą, podyskutować, zadać pytanie?

Alicja Kukla-Kowalska expert FORDATA

Poprzednie raporty fuzji i przejęć w Polsce

![]()

Jest czołowym dostawcą usługi Virtual Data Room w Polsce i w regionie CEE. Rozwiązanie FORDATA VDR wspiera największe transakcje M&A, IPO, inwestycje Private Equity i prywatyzacje.

W oparciu o autorskie systemy informatyczne, bazujące na technologii Virtual Data Room, pomaga klientom w zarządzaniu dokumentami i komunikacją podczas złożonych procesów transakcyjnych.

Współpracuje z liderami branż, w tym największymi firmami doradczymi, kancelariami prawnymi, bankami, czy funduszami PE/VC z całego świata. FORDATA zrealizowała dotychczas ponad 500 transakcji podnosząc bezpieczeństwo i efektywność projektów o łącznej wartości ponad 40 mld PLN.

![]()

Wraz z Domem Maklerskim Navigator jest czołowym niezależnym doradcą finansowym dla przedsiębiorstw specjalizującym się w transakcjach M&A oraz publicznych i prywatnych emisjach akcji i obligacji. W ciągu ostatnich lat Grupa Navigator zrealizowała ponad 35 transakcji różnego typu.

Partnerzy Navigator przeprowadzili transakcje o łącznej wartości ponad 6,2 mld PLN. Współpraca z międzynarodową siecią firm doradczych zrzeszonych pod szyldem Pandion Partners pozwala skutecznie obsługiwać transakcje międzynarodowe.

Navigator Capital wraz z Domem Maklerskim Navigator zajmują wysokie pozycje w niezależnych rankingach oceniających aktywność podmiotów doradczych na rynku polskim.