M&A Index Poland

3 kwartał 2017

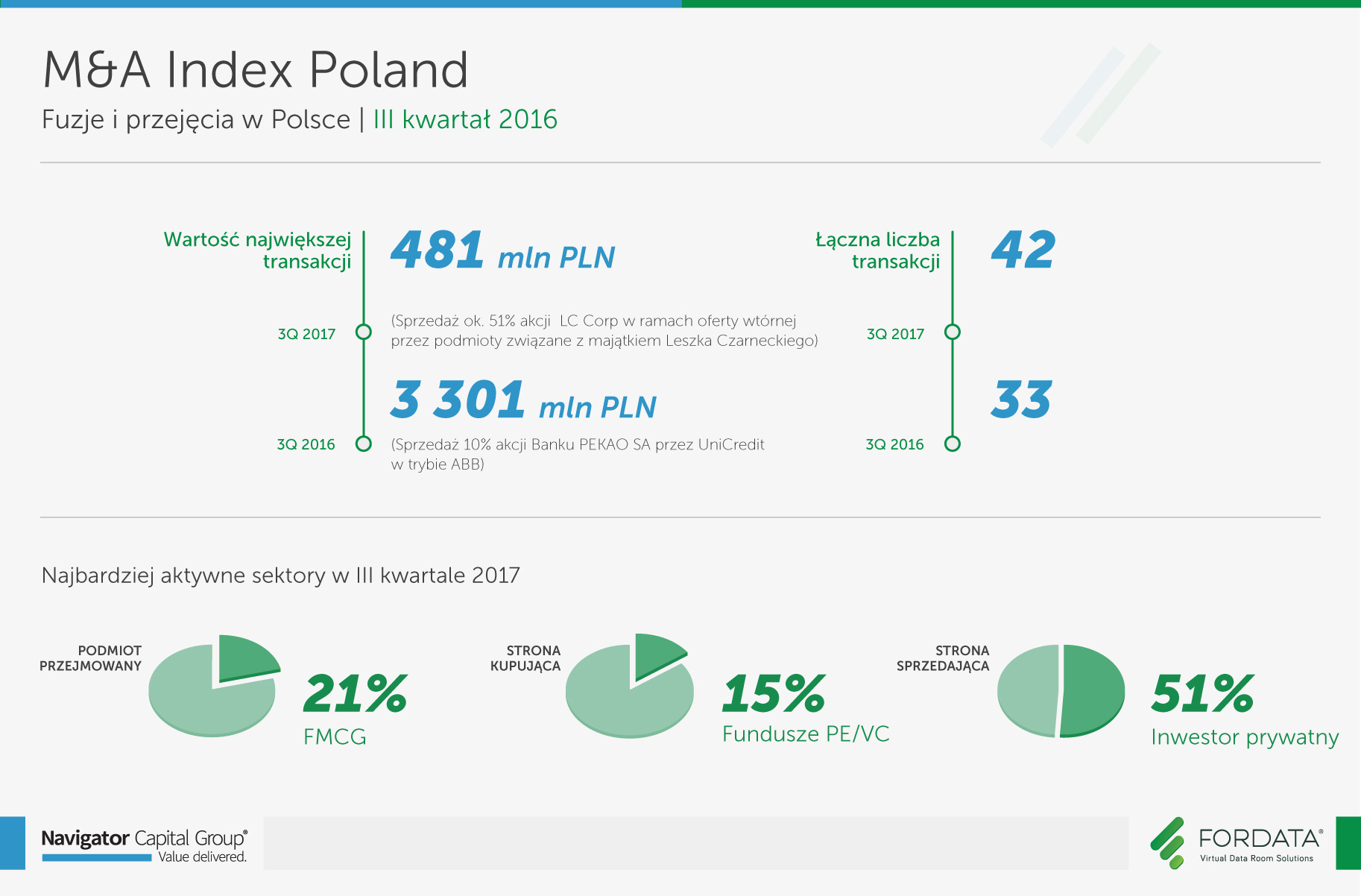

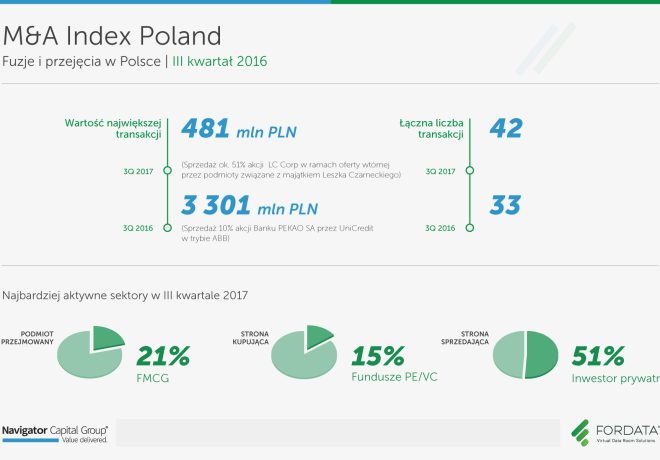

42

łączna liczba transakcji

481 mln

wartość największej transakcji (PLN)

33%

popularność Virtual Data Room

Zgodnie z naszym przewidywaniem, odsetek prywatnych przedsiebiorców po stronie sprzedających wzrósł i wrócił do wartości obserwowanych na początku roku (wzrost z 27% do 52% Q2/Q3). Najwięcej transakcji miało miejsce w FMCG oraz branży Media/IT/Telecom (odpowiednio 21% i 17%). Po stronie kupującej dominują spółki z funduszy PE/VC (15%) oraz branży Media/IT/Telecom (13%). Fundusze nie przestaja tez sprzedawać, choc ilość wyjść z inwestycji zmalała w porównaniu do 2 kwartału. Enterprise Investors odchudził swój portfel o kolejna w tym roku spółkę - Elemental Holding, a najciekawszym wyjściem była sprzedaż sieci supermarketów Mila przez Argus Capital do Eurocash za 350 mln złotych. Była to też druga co do wielkości transakcja tego kwartału. Due diligence zostało zorganizowane z wykorzystaniem technologii Virtual Data Room dostarczanej przez FORDATA. Wykorzystanie podczas transakcji technologii Virtual Data Room, która gwarantuje bezpieczne udostępnianie poufnych dokumentów drugiej stronie procesu utrzymuje sie na stabilnym poziomie. Z dostępnych danych wynika, ze w 3 kwartale 33% transakcji zostało zrealizowanych z wykorzystaniem systemu Virtual Data Room.

Chcesz wymienić się wiedzą, podyskutować, zadać pytanie?

Alicja Kukla-Kowalska expert FORDATA

Poprzednie raporty fuzji i przejęć w Polsce

![]()

Jest czołowym dostawcą usługi Virtual Data Room w Polsce i w regionie CEE. Rozwiązanie FORDATA VDR wspiera największe transakcje M&A, IPO, inwestycje Private Equity i prywatyzacje.

W oparciu o autorskie systemy informatyczne, bazujące na technologii Virtual Data Room, pomaga klientom w zarządzaniu dokumentami i komunikacją podczas złożonych procesów transakcyjnych.

Współpracuje z liderami branż, w tym największymi firmami doradczymi, kancelariami prawnymi, bankami, czy funduszami PE/VC z całego świata. FORDATA zrealizowała dotychczas ponad 500 transakcji podnosząc bezpieczeństwo i efektywność projektów o łącznej wartości ponad 40 mld PLN.

![]()

Wraz z Domem Maklerskim Navigator jest czołowym niezależnym doradcą finansowym dla przedsiębiorstw specjalizującym się w transakcjach M&A oraz publicznych i prywatnych emisjach akcji i obligacji. W ciągu ostatnich lat Grupa Navigator zrealizowała ponad 35 transakcji różnego typu.

Partnerzy Navigator przeprowadzili transakcje o łącznej wartości ponad 6,2 mld PLN. Współpraca z międzynarodową siecią firm doradczych zrzeszonych pod szyldem Pandion Partners pozwala skutecznie obsługiwać transakcje międzynarodowe.

Navigator Capital wraz z Domem Maklerskim Navigator zajmują wysokie pozycje w niezależnych rankingach oceniających aktywność podmiotów doradczych na rynku polskim.