Raport Fuzje i przejęcia w Polsce

3 kwartał 2018

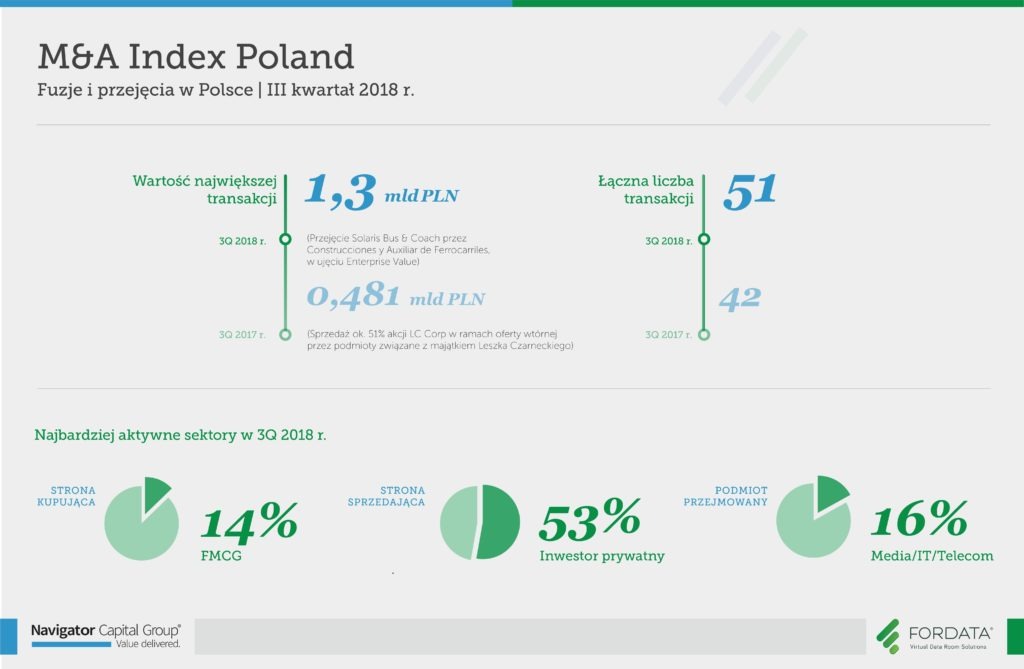

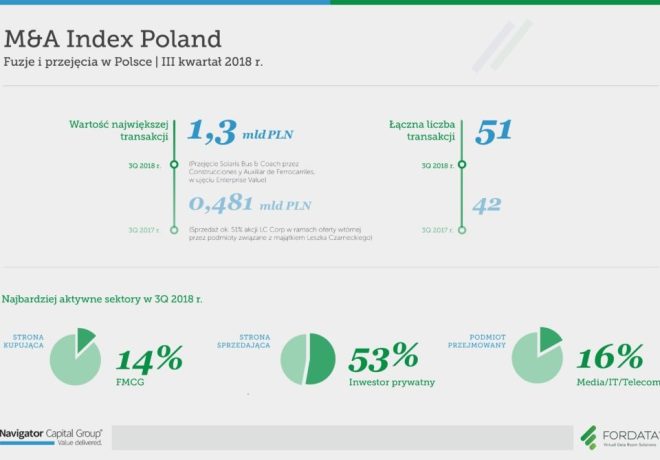

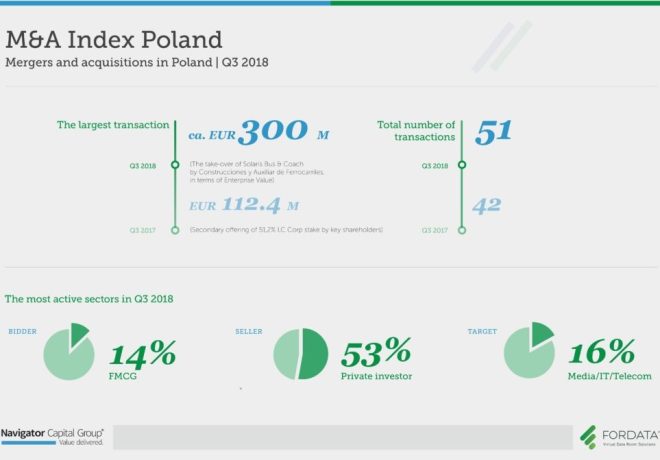

51

łączna liczba transakcji

1.3 MLD

wartość największej transakcji (PLN)

Z dostępnych danych wynika, że tylko 5 spośród 32 transakcji było zorganizowanych z użyciem systemu typu Virtual Data Room (VDR). Pomimo tego, że w branży panuje opinia, że VDR jest standardem wykorzystywanym do profesjonalnej organizacji transakcji, wciąż niewielu przedsiębiorców, czy doradców transakcyjnych chwali się użyciem tego narzędzia. Tymczasem jest to powód do dumy, bo VDR to synonim bezpiecznego zarządzania poufnymi informacjami, profesjonalne podejście do prowadzonych transakcji, a także znaczne przyśpieszenie procesów M&A. System typu Virtual Data Room (VDR) to aplikacja dostępna przez Internet, która służy do zarządzania poufnymi dokumentami i komunikacją podczas złożonych i poufnych transakcji. Umożliwia ona realizację transakcji w formie elektronicznej, skracając jej czas, podnosząc efektywność oraz gwarantując pełną kontrolę i bezpieczeństwo przekazywanych informacji. Oferowana jest w formie usługi, udostępnianej na określony czas, wraz z profesjonalnym doradztwem w zakresie właściwej organizacji procesu. W kolejnych odsłonach raportu będziemy pilotować częstotliwość jego wykorzystania podczas transakcji M&A w Polsce.

Chcesz wymienić się wiedzą, podyskutować, zadać pytanie?

Alicja Kukla-Kowalska Key Account Manager FORDATA

Poprzednie raporty fuzji i przejęć w Polsce

![]()

Jest czołowym dostawcą usługi Virtual Data Room w Polsce i w regionie CEE. Rozwiązanie FORDATA VDR wspiera największe transakcje M&A, IPO, inwestycje Private Equity i prywatyzacje.

W oparciu o autorskie systemy informatyczne, bazujące na technologii Virtual Data Room, pomaga klientom w zarządzaniu dokumentami i komunikacją podczas złożonych procesów transakcyjnych.

Współpracuje z liderami branż, w tym największymi firmami doradczymi, kancelariami prawnymi, bankami, czy funduszami PE/VC z całego świata. FORDATA zrealizowała dotychczas ponad 500 transakcji podnosząc bezpieczeństwo i efektywność projektów o łącznej wartości ponad 40 mld PLN.

![]()

Wraz z Domem Maklerskim Navigator jest czołowym niezależnym doradcą finansowym dla przedsiębiorstw specjalizującym się w transakcjach M&A oraz publicznych i prywatnych emisjach akcji i obligacji. W ciągu ostatnich lat Grupa Navigator zrealizowała ponad 35 transakcji różnego typu.

Partnerzy Navigator przeprowadzili transakcje o łącznej wartości ponad 6,2 mld PLN. Współpraca z międzynarodową siecią firm doradczych zrzeszonych pod szyldem Pandion Partners pozwala skutecznie obsługiwać transakcje międzynarodowe.

Navigator Capital wraz z Domem Maklerskim Navigator zajmują wysokie pozycje w niezależnych rankingach oceniających aktywność podmiotów doradczych na rynku polskim.